PWC in its latest Asset & Wealth Management Industry whitepaper predicts assets to go from $85T to $145T in the next decade – why the authors would call it almost doubling the assets I am not sure (and I am sure plenty of firms would like to get a piece of the $25T rounding error), but let’s go with significant growth overall globally.

The report points to four (or more) main trends that will promote and challenge the business:

– Downward fee pressure by regulators and the industry (we discussed the unintended business model consequences of regulation at our CSI roundtables last month).

– Increased regulation (against commission payments) revolutionizing wealth managers’ raison d’etre.

– Technology changes will drive “quantum change across the value chain” for the “digital technology laggard” (similarly, we discussed a lot of the data and technology challenges for asset and wealth managers in NY, Boston, Paris and London, but I am not sure the industry is as far behind technologically as many make it out to be.

– Asset managers will continue to increase their involvement in trade finance, peer-to-peer lending and infrastructure to equip individuals to save for old age. An interesting thesis and I would agree with the continued innovation post-crisis for the industry with asset managers as demand-based first movers.

– A big focus on outcomes with the need to focus on core capabilities and outsource non-core functions such as tax compliance. The focus on outcomes is undisputed, along with the demand for alternatives and passive investments. However, I am not sure calling active management and growth opportunities in question is called for. True, active management has been challenged mightily since the crisis (and even before), but aside from some of the very large-cap strategies, managers have been able to continuously find value for clients and grow/sustain their businesses. More debate ahead, of course.

– People: “firms must find and develop people with new skills and adapt their employment models to nurture and retain them.” Agreed. A lot of change is under way for the industry, especially inasmuch as data gathering, securing, monitoring and analyzing is moving front and center for legal, operational, risk, compliance and business functions.

A few of the other interesting nuggets that stood out when discussing the asset and wealth management landscape, especially with its implications for compliance, legal and risk functions, are:

– Alternative asset classes will more than double in size (esp real assets, private equity and private debt)

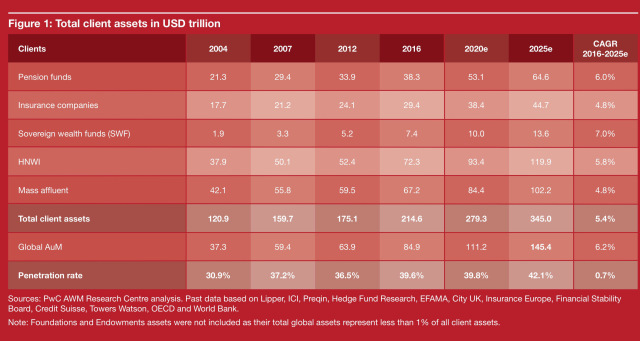

– Managed asset penetration rates will go from 39.6% to 42.1%

– Challenges including geopolitics, Brexit, China moving to consumer-driven economy, potential US policy changes

– Highest growth rates in Asia and Latin America

– Fee pressure will rise with Mifid 2 pushing asset managers’ costs up and banning wealth managers‘ retrocession

– Brexit could cause major disruptions to the European industry

– Transparency impact with Mifid 2 and DOL Fiduciary Rule, CRS, et al

Bottom line: the industry will continue to grow, complexity will increase, and regulation and compliance will drive business models and growth.